Introduction

Long-term saving is hardest when income changes and family expectations do not. One month may include extra hours, another may be tight, and a third may bring an unexpected local expense. Many workers do not fail because they are careless. They fail because their saving plan assumes a stable life that they do not actually have.

Long-term saving becomes difficult when income moves up and down but your responsibilities do not. Family support continues, bills continue, and tired decisions can eat the very money you hoped would become a future plan.

Build a rule that survives real months

A strong long-term habit is usually quieter than people expect.

It is not built on one perfect month. It grows because the rule is realistic enough to survive:

- Weak months

- Strong months

- Financial pressure

Fixed promises often collapse.

A flexible rule lasts longer.

Examples:

- Save a percentage of income

- Save a base amount + part of overtime

What long-term savings are really protecting

Long-term savings are not only for one purchase.

They protect:

- Returning home with stability

- Supporting family goals

- Education

- Future business plans

- Life after working abroad

When money has a clear purpose, it is easier to protect.

Separate long-term saving from emergency saving

These are different:

- Emergency money = short-term protection

- Long-term savings = future planning

If they are mixed:

- Both can disappear during pressure

Even small separation is powerful.

How uncertain income changes the strategy

Do not build your plan based on your highest income month.

Instead:

- Use average income as base

- Use strong months to increase savings

Example:

- Save regular amount monthly

- Save extra when overtime comes

Turn extra income into progress

Overtime and extra income should not disappear.

Set a rule:

- Part of extra income goes directly to savings

This turns unstable income into long-term growth.

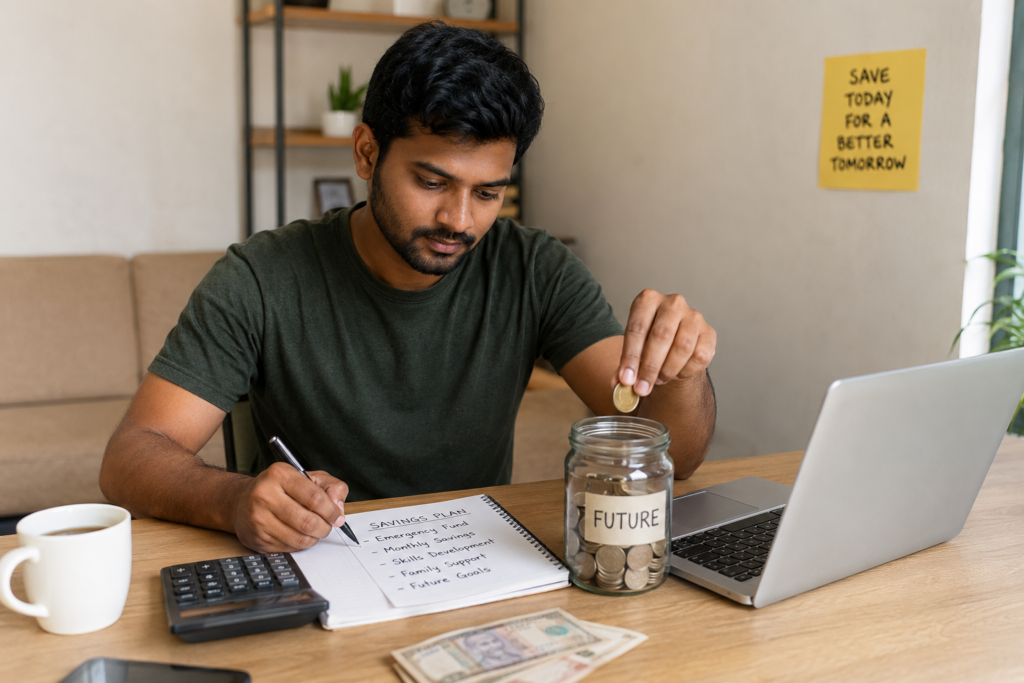

Make progress visible

People protect what they can see.

Track your savings:

- Notebook

- App

- Spreadsheet

Show:

- Current amount

- Goal

- Progress

This helps motivation and communication.

Real-life examples

One worker saved only during “good months” and made little progress.

Another used a percentage rule and stayed consistent.

A third used overtime as a trigger for saving and built progress faster.

Conclusion

Long-term saving with uncertain income is about:

- Flexibility

- Consistency

- Realistic planning

Small, steady progress is stronger than big promises.

Final Tip

Do not wait for stability to start saving —

build a system that works even without it.