Many foreign workers in Israel hear the words “National Insurance” but do not fully understand what they mean in daily life. Some workers think it is the same as private medical insurance. Others think it is a deduction that disappears into the system and has no real value. Both ideas are incomplete.

In Israel, National Insurance is a legal reporting and payment system connected to specific social protections. For foreign workers, the rules are not identical to the rules that apply to Israeli residents. This is exactly why the topic creates confusion.

A foreign worker may see deductions on the payslip, may hear that the employer “opened a file,” or may be told that private health insurance already covers everything. In practice, each of these points is only one part of the picture. A worker needs to know what National Insurance covers, what it does not cover, who must report, and what documents should be checked every month.

This article explains the subject in plain English for website publication and later Sinhala translation. It is written to help workers ask better questions, keep the right records, and understand the difference between legal payroll reporting and private medical coverage.

Why this topic matters

National Insurance matters because a problem usually appears only when the worker needs help. A person may work for months or years without thinking about it. Then an accident happens, a pregnancy issue arises, a salary dispute starts, or an employer disappears. At that moment, correct reporting becomes very important.

This topic also matters because many workers wrongly assume that if money was deducted from salary, everything must be correct. That is not always true. A deduction line on a payslip is not the same as proper reporting to the authorities. A worker should understand that paperwork, reporting, and payment history all matter.

For Sri Lankan workers and other migrant communities, the issue is even more sensitive because information often passes through friends, agents, translators, or social media groups. Helpful advice can circulate, but mistakes also spread quickly. A clear article reduces fear and replaces rumors with a basic working structure.

What National Insurance means for a foreign worker

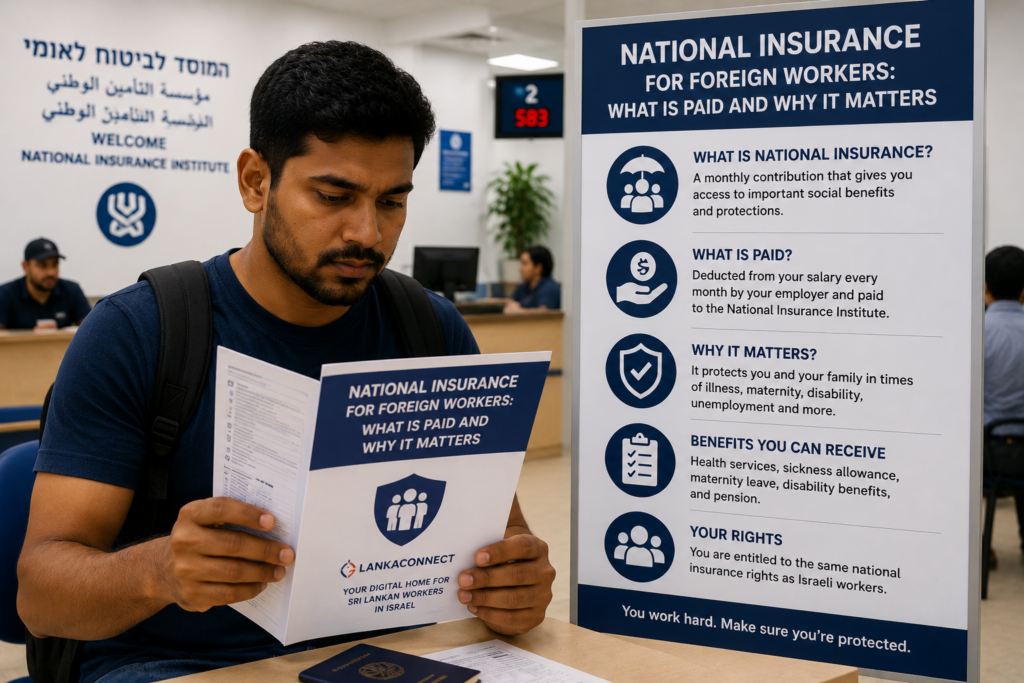

For a foreign resident employee in Israel, the employer generally has a duty to report the worker and pay National Insurance contributions for the branches that apply to foreign residents. Official National Insurance guidance explains that foreign residents are not covered by state health insurance under Israeli law, but employers must pay for specific branches such as work injury, bankruptcy protection, and maternity insurance where relevant. This is why private medical insurance is still required separately for many foreign workers.

This point is critical: National Insurance and private health insurance are not the same product. Private medical insurance is usually arranged to cover healthcare needs because foreign workers do not receive the same public health coverage as Israeli residents. National Insurance, by contrast, relates to legal social-insurance branches defined by law and connected to events such as work injury and other protected situations.

So when a worker asks, “Am I insured?” the real answer may be split into two parts: one answer about National Insurance, and another answer about private medical insurance. A worker should not confuse them.

Who is responsible for reporting and payment

In normal employee-employer relationships, the employer is the party responsible for reporting the worker and paying the required contributions. This applies even if the worker is employed in a private household, such as caregiving or domestic work. The worker should not assume that silence means compliance. The safest approach is to ask for written proof that reporting exists and then compare that claim with the payslip and any official records that can be obtained.

If a worker has more than one employer, each employment relationship may create separate reporting questions. If a worker changes employers, there may also be a gap risk between one workplace and the next. That is why employment start dates and end dates should be saved carefully.

Workers should also understand that an employer cannot simply say, “I gave you private insurance, so I do not need to report you.” These are different legal issues. Private coverage does not replace the employer’s National Insurance duties.

What a worker should check every month

A good monthly review takes only a few minutes and can prevent bigger problems later. First, review the payslip. Look for the worker’s name, employer name, salary period, gross salary, deductions, and net pay. If National Insurance appears, note the amount and keep the slip.

Second, compare the payslip with the bank transfer or payment proof. The amount received should match the net salary unless there is a clear and documented reason for a difference.

Third, keep copies of the private medical insurance card or policy, passport, visa documents, work schedule, and any messages about leave, injury, or unpaid days. National Insurance questions become easier to solve when all records sit in one folder.

Fourth, if something changes suddenly, ask in writing. A short message is enough: “Please confirm whether I am reported correctly for National Insurance and explain this month’s deduction line.” Short written questions are better than emotional arguments.

What rights may connect to this system

The exact right depends on the event and on the worker’s legal situation, but the most important practical areas usually include work injuries, maternity-related issues where relevant, and protection connected to employer bankruptcy or liquidation. A worker does not need to memorize every legal detail. It is more important to understand that these protections exist and that correct employer reporting may become decisive when a claim is examined.

For example, if a worker is injured while working or while traveling in circumstances that legally qualify as a work injury, documentation becomes essential. Medical documents, incident details, witness names, and immediate reporting can all affect the ability to make a claim later.

In maternity-related situations, timing and paperwork matter. Even where a possible benefit exists in principle, the claim still has to fit the legal conditions. A worker should therefore gather documents early and avoid relying only on verbal advice.

Common confusion points

One common confusion is the belief that if National Insurance is on the payslip, then all legal duties were completed perfectly. That may be true, but it is not guaranteed. Payslip entries are important evidence, not final proof of the entire legal process.

Another confusion point is the idea that foreign workers receive exactly the same social-insurance package as Israeli residents. The official guidance shows that foreign residents are treated differently in important areas, especially in relation to state health coverage. Workers should therefore avoid copying advice that was written for Israeli citizens or permanent residents without checking whether it also applies to foreign residents.

A third confusion point is the belief that this issue matters only for big factories or large employers. In reality, private employers, households, and small workplaces can also create problems if reporting is ignored or handled badly.

Practical example 1: injured at work

A caregiver slips while helping a patient move from bed to chair and injures her back. She goes to a clinic, receives treatment, and rests for several days. If she has no records, no written report, and no saved payslips, proving the work connection later may become harder. A better response is to seek medical care immediately, report the event in writing, save the clinic documents, and keep the salary records for the same period.

This example shows why National Insurance is not an abstract topic. It becomes real when income, treatment, and legal rights meet in one moment.

Practical example 2: employer says private insurance is enough

A worker asks whether National Insurance is paid. The employer answers: “Do not worry, I already bought your health insurance.” That answer sounds reassuring, but it does not solve the actual question. Private health insurance and National Insurance are different. The worker should politely ask again for confirmation of National Insurance reporting and keep the reply in writing.

Practical example 3: changed employers

A worker finishes one job at the end of June and begins a new job in mid-July. During this transition, a paperwork gap appears. Later, the worker needs proof about the employment period. Because she saved the release message from the first employer, the new contract, the visa documents, and the first payslip from the new job, it becomes easier to explain the timeline.

Common mistakes to avoid

Do not assume that a missing problem means everything is correct. Many payroll or reporting issues stay invisible until a crisis starts.

Do not depend only on spoken promises. A written message, payslip, or official document is stronger than memory.

Do not mix National Insurance with private health insurance in conversation. Ask about each one separately.

Do not throw away old payslips. Even older slips can become important evidence.

Do not wait too long after an injury, deduction problem, or employer dispute. Delay can damage a future claim.

Simple worker checklist

Keep every monthly payslip in digital form.

Save bank transfer proof or salary receipt every month.

Keep a copy of private medical insurance separately from payroll records.

Write down every employer start date and end date.

After any accident, save medical papers and send a short written report.

If something is unclear, ask one precise written question instead of many vague questions.

How to speak to the employer professionally

A calm message usually works better than a long complaint. Example: “Hello, I am organizing my records. Please confirm that I am reported correctly for National Insurance and explain the deduction line on my payslip. Thank you.”

If the issue is about an injury, be even more specific: “I was injured on [date] during work. I received treatment at [clinic/hospital]. Please confirm the reporting process and what documents you need from me.”

These messages are simple, respectful, and easy to translate. They also create a written timeline.

Conclusion

National Insurance for foreign workers in Israel is a practical protection issue, not just a payroll detail. It affects what happens when work is interrupted, when an accident occurs, or when an employer fails in legal duties.

The most important ideas are simple: National Insurance is not the same as private health insurance, the employer usually has the reporting duty, and every worker should keep payslips, payment proof, and key documents in one organized folder.

Workers do not need to become lawyers. They only need a good habit: check the payslip, save the records, and ask clear written questions early. That habit protects money, confidence, and rights.